Over the past decade, Environmental, Social and Governance (ESG) scores have become an important measure in investment decision-making, corporate reporting, and sustainability strategy. Investors rely on ESG scores to evaluate a firm’s sustainability performance, regulators encourage publishing the scores for transparency, and businesses use them to highlight their commitment to responsible practices. Yet a fundamental challenge persists: Why do ESG scores for the same company differ widely across ESG Rating Providers (ERPs)? A company that appears strong on LSEG/Refinitiv may receive a much weaker score from providers like CRISIL or ICRA, while another provider, Bloomberg, may place the same firm somewhere in-between. These inconsistencies affect investor confidence, complicate regulatory oversight, and weaken the credibility of ESG scores as a tool for sustainable development.

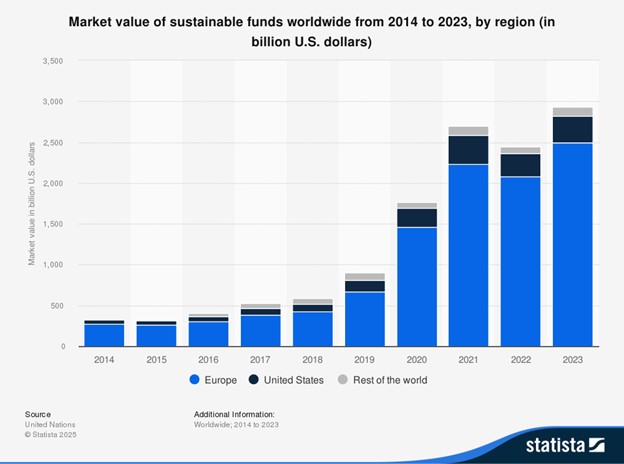

Figure 1: Market value of sustainable funds worldwide, by region

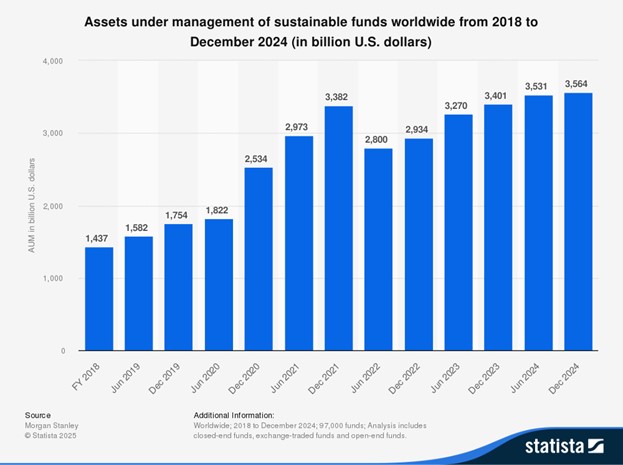

The past decade has witnessed a significant surge in susbtainable funds worldwide. Figure 1 shows that the global market value of sustainable funds increased from USD 326 billion to nearly USD 3 trillion, between 2014 and 2023, with Europe leading in ESG-aligned assets. Figure 2 shows that there has been a significant expansion of global sustainable funds in recent years in terms of the total assets under management of various fund houses. After rising consistently between 2018 and 2021 and reaching their highest point by the end of 2021, they experienced a temporary decline to about USD 2.8 trillion in mid-2022. However, this decline was short-lived, as sustainable fund AUM rebounded, climbing to approximately USD 3.56 trillion by December 2024.

Figure 2: Assets under management of sustainable funds worldwide

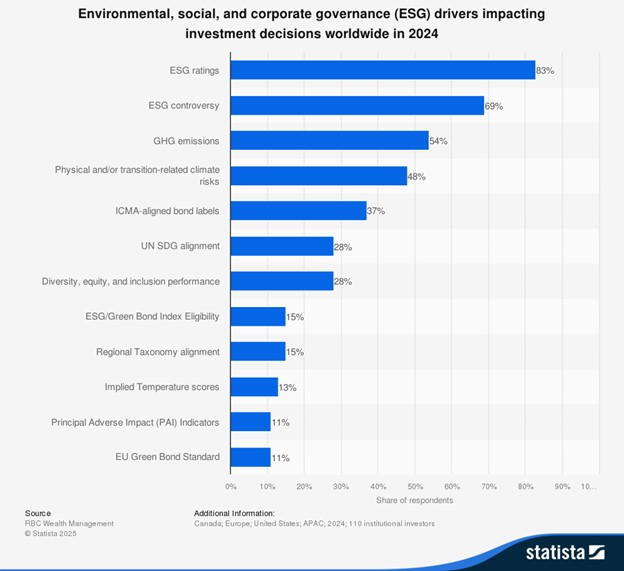

Figure 3: ESG drivers impacting investment decisions worldwide

A survey conducted on institutional investors revealed that ESG ratings had become one of the most influential inputs guiding investment choices worldwide, as presented in Figure 2. Over four-fifths of institutional investors identified ESG scores as a primary factor shaping their investment decisions. Nearly seven in ten investors consider ESG-related controversy scores. In comparison, only a small share-around 11 percent-reported that the EU Green Bond Standard influenced their investment approach. According to a survey in 2023, a growing proportion of private equity (PE) investors are incorporating ESG considerations into their investment strategy. The survey results showed that 61 percent of PE investors consider ESG as a determining factor in their investment strategies.

Despite this momentum, there is a lack of consistency in ESG methodologies. Among US ETF investors, methodological concerns remain the most highlighted reason for avoiding ESG-themed investment products. The absence of a unified framework makes it difficult for investors to rely on ESG ratings with certainty for investments. These methodological concerns have directly shaped regulatory reforms in India.

In India, the Securities and Exchange Board of India (SEBI) has moved decisively to address these issues. SEBI publicly raised concerns regarding methodological inconsistencies and the unregulated dissemination of ESG scores by global data platforms. This resulted in the withdrawal of ESG scores published on Indian firms by LSEG/Refinitiv and Bloomberg, as these entities were not registered as ERPs under SEBI’s regulatory framework. The SEBI Master Circular for ESG Rating Providers, issued on July 11, 2025, provides a comprehensive governance structure that mandates registration, transparency, and accountability for all ERPs operating in the Indian market. The circular explicitly outlines requirements related to registration (Chapter I), rating operations, disclosure norms, business models, governance, and rules governing suspension, cancellation, and withdrawal of ESG ratings (pp. 6–13) . These regulatory changes represent a fundamental turning point: ESG ratings, once distributed freely by global platforms without domestic oversight, now fall squarely within India’s regulated financial ecosystem.

The mandatory registration requirement under the amended SEBI Regulations means that ESG scores marketed as opinions on a company’s environmental, social, governance, or transition performance cannot be published without a SEBI-issued ERP licence. Chapter I of the Master Circular specifies the requirements of ERP registration, while Chapter II defines allowable rating types, including ESG Rating, Transition Score, Combined Score, and Core ESG Rating (pp. 14–17). The circular also mandates that all ESG scores must follow transparent methodologies, adhere to clear rating scales (0–100), disclose rating rationales, and maintain strict conflict-of-interest controls. It is under this new regulatory framework that LSEG/Refinitiv and Bloomberg withdrew their Indian ESG scores, as they were not registered ERPs and therefore not authorised to publish such ratings.

Understanding why ESG scores diverge is essential for their interpretation. Prior research and regulatory reviews shows that differences across ESG rating providers arise mainly from variations in data sources, treatment of missing disclosures, application of materiality frameworks, sector-relative versus absolute scoring approaches, and the manner in which ESG controversies are incorporated into ratings. These methodological choices together explain much of the observed inconsistency in ESG scores across providers (Berg et al., 2022; OECD, 2020; IOSCO, 2021). A brief comparison highlights these differences. LSEG/Refinitiv uses a data-driven approach grounded in numerous public-domain indicators and applies sector-relative scoring, which can obscure local contextual performance (LSEG, 2024). CRISIL, by contrast, emphasises ESG risk from a credit-relevance perspective, integrating industry-specific KPIs, forward-looking governance assessments, and India-specific regulations into its methodology (CRISIL, 2023). ICRA similarly integrates ESG considerations into credit-risk assessment tools for domestic debt markets, blending quantitative metrics with qualitative governance analysis (ICRA, 2024). These methodological differences mean that the same company’s ESG performance can be interpreted in fundamentally different ways by different providers.

This divergence also increases the risk of greenwashing, an issue that SEBI explicitly acknowledges. Greenwashing occurs when companies or funds misrepresent their ESG performance, through selective disclosure, inadequate assurance, or reliance on unverified claims. SEBI’s regulatory response has been multi-layered. For ESG mutual funds, SEBI has enhanced disclosure norms, required clear investment policies, mandated stewardship transparency, and introduced BRSR-based investment thresholds. These changes are made to ensure alignment between fund names, stated strategies, and actual holdings. In the context of corporate disclosures, greenwashing risks arise when companies disclose non-assured sustainability data that rating providers then incorporate into scores. SEBI’s requirement that Core ESG Ratings must rely solely on third-party assured data (Master Circular, p. 16) is a direct response to such risks. SEBI’s stronger governance rules, clarity on conflict-of-interest management, and mandated disclosure of methodologies further protect investors from misleading sustainability claims.

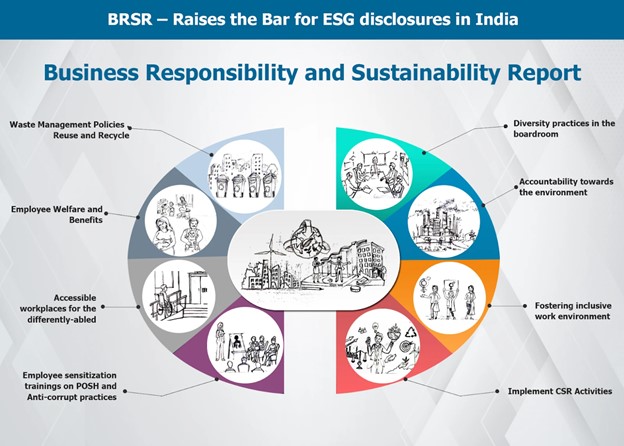

Figure 4: Business Responsibility and Sustainability Report (BRSR)

At the corporate reporting level, India’s transition from Business Responsibility Reporting (BRR) to the more comprehensive Business Responsibility and Sustainability Report (BRSR) represents another major reform. BRSR is introduced as a mandatory requirement for the top 1,000 listed companies from FY 2022–23, ensures standardised, comparable ESG disclosures across firms. From FY 2023–24 onwards, BRSR Core requires third-party assurance of select metrics, significantly raising the credibility of India’s sustainability reporting ecosystem. This directly supports ERP functioning, as it provides verified, high-quality inputs for rating models.

The integration of India-specific ESG parameters into ERP methodologies is mandated under Annexure 3 of the Master Circular (pp. 50–52) . These include compliance with national environmental laws, PAT scheme targets, Zero Liquid Discharge practices, EPR compliance, and region-specific water-risk factors, among others. SEBI requires ERPs to reflect India’s social and regulatory realities, such as MSME sourcing, CSR utilisation, and governance dynamics. This is to ensure that the ratings better represent Indian operating conditions rather than relying purely on global benchmarks.

Greenwashing concerns also intersect with the wide divergence in ESG scores across providers. When companies or funds selectively highlight favourable ratings while ignoring weaker ones, they distort stakeholder perception. SEBI’s rules on rating rationale disclosures, rating sensitivity factors, and mandated explanation for rating changes (pp. 21–23) ensure that investors have full visibility into what drives ESG ratings, making it harder for firms to misrepresent their sustainability position. Moreover, ERPs must maintain robust internal audit systems and governance committees (p. 39), reinforcing independence and analytical integrity.

Taken together, these reforms mark a structural shift in India’s ESG landscape. Companies must now prioritise assured disclosures, accurate data, and long-term risk management practices rather than treating ESG as a public-relations exercise. Investors, meanwhile, are encouraged to treat ESG scores not as definitive signals but as an indicator that must be interpreted alongside BRSR disclosures, sectoral dynamics, and corporate governance quality. Regulators have signalled that sustainable finance in India must be grounded in reliable data, transparent methodologies, and accountability from rating providers.

References

SEBI Master Circular for ESG Rating Providers (2025), https://www.sebi.gov.in/legal/master-circulars/jul-2025/master-circular-for-esg-rating-providers-erps-_95219.html

Vinod Kothari article on ERPs, https://vinodkothari.com/2023/04/regulating-esg-rating-providers-in-india/#:~:text=Current%20position%20of%20ERPs%20in,available%20on%20a%20subscription%20basis.

ESG Scores from LSEG (2024), https://www.lseg.com/content/dam/data-analytics/en_us/documents/methodology/lseg-esg-scores-methodology.pdf

CRISIL’s ESG Scoring Methodology (2023), https://www.crisil.com/content/dam/crisil/our-businesses/india_research/sustainability-yearbook-2022/methodology/crisil-esg-methodology.pdf

ICRA’s Impact rating Methodology (2024), https://www.icraesgratings.in/Ratings/ShowImpactRatingMethodology

Berg, F., Kölbel, J. F., & Rigobon, R. (2022). Aggregate confusion: The divergence of ESG ratings. Review of Finance, 26(6), 1315-1344.

IOSCO (2021). ESG Ratings and Data Products Providers.

OECD (2020). ESG Investing: Practices, Progress and Challenges.

Copyright © 2026. Rajagiri Business School. All Rights Reserved. Website Designed and Maintained by Intersmart